5 Ways to Save Money on Travel Insurance

Travel insurance isn’t an exciting way to spend your trip budget, but you might as well save some money

7 October 2011

Travel costs can add up, so you should save money on travel insurance if you can. You still want the right coverage for your trip, but here are some rules to help you get the right plan and save some cash.

1. Don’t ‘opt-in’ on booking sites

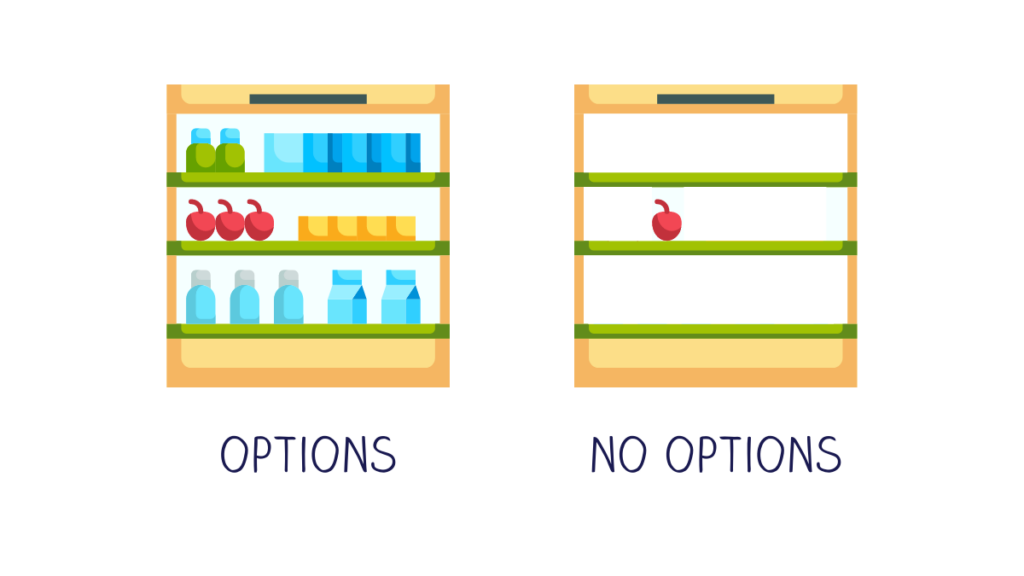

It looks easy, but skip the checkbox for travel insurance on booking sites like Kayak, Expedia, or cruise line sites. Here’s why:

You won’t read the policy details because you are focused on something else. You’re in the mindset of picking the right seat on your plane. Or going through the details of your cruise. Make insurance a separate decision when you can focus.

More importantly, you don’t have any choices when you use the opt-in. The travel supplier makes a deal with one travel insurance company. To offer one plan. This plan will often be stripped-down to keep the cost low, but you miss out on important coverage.

Rule #1: You’ll have more focus, selection, and ability to purchase upgrades if you use a travel insurance comparison engine instead.

2. Don’t over-insure your trip

Travel insurance covers your trip costs if you need to cancel. Trip costs are any pre-paid, non-refundable trip expense.

If you insure trip costs that are refundable, you will not be paid back for this if you make a claim. That would mean you could get our refund, and get paid by the insurance company.

Only insure trip costs that are pre-paid, and non-refundable (for cash, not credit or vouchers).

How about credits or vouchers? If you need to cancel your trip, the travel supplier might offer you a credit or voucher. To collect insurance, you would need to refuse the voucher from the supplier. Then you would receive cash reimbursement from the travel insurance company.

Rule #2: Only insure the trip costs that are non-refundable and pre-paid.

3. Avoid sky-high coverage limits

Emergency medical coverage is important if you’re leaving your home country. There are plans with emergency medical limits of $500,000. That is a lot of coverage. Unless you have specific needs, don’t get too focused on the high coverage limits.

For reference: With cruise trips, it is recommended you get a minimum of $100,000 of coverage. That’s because cruises are unique trips that take you far from hospitals.

Emergency evacuation coverage can see limits at high as $2,000,000. Again, this is overdone.

Rule #3: Avoid over-insuring your emergency medical & evacuations ($250,000 to $500,000 is adequate)

4. Compare plan to save money on travel insurance

Rule #1 above talks about avoiding the opt-in coverage when you book. That’s because you only get one option to choose from.

The opposite of that is using a comparison site (like CoverTrip) to get quotes from all companies in the same place. This lets you see coverage and pricing side-by-side so you can find the best pricing.

The cost is the same wherever you purchase because insurance is regulated. You might as well comparison shop to save money on travel insurance.

Rule #4: Use a comparison site to find the best price instead of having one option.

5. Don’t assume cheaper means worse coverage

Travel insurance policy rates are a mystery. You will see two plans that seem like they have equal coverage, but one will be twice as expensive.

Insurance companies have target demographics for their insurance products. They tweak rates to appeal to their target market.

This means you might find a plan that fits your needs, but it’s less expensive than similar plans. This just means their rating was optimized for a different demographic. Save money on travel insurance and buy the cheapest plan that fits your needs.

Rule #5: Find the coverage you need, make sure it’s enough coverage, then buy based on price.

More helpful links:

DamianTysdal

Damian Tysdal is the founder of CoverTrip, and is a licensed agent for travel insurance (MA 1883287). He believes travel insurance should be easier to understand, and started the first travel insurance blog in 2006.

Damian Tysdal is the founder of CoverTrip, and is a licensed agent for travel insurance (MA 1883287). He believes travel insurance should be easier to understand, and started the first travel insurance blog in 2006.